Canada

Canada

US

US

You are now leaving our website and entering a third-party website over which we have no control.

Flexible Mortgage Payment Features

TD Mortgages have flexible payment options and can help you prepare for the unexpected. Whether you’re having a baby or your financial needs grow and change over time, TD Mortgages help you prepare for the unexpected with a range of flexible payment features to suit you.

-

Speed Up Your Payments

-

Slow Down Your Payments

-

Prepayments

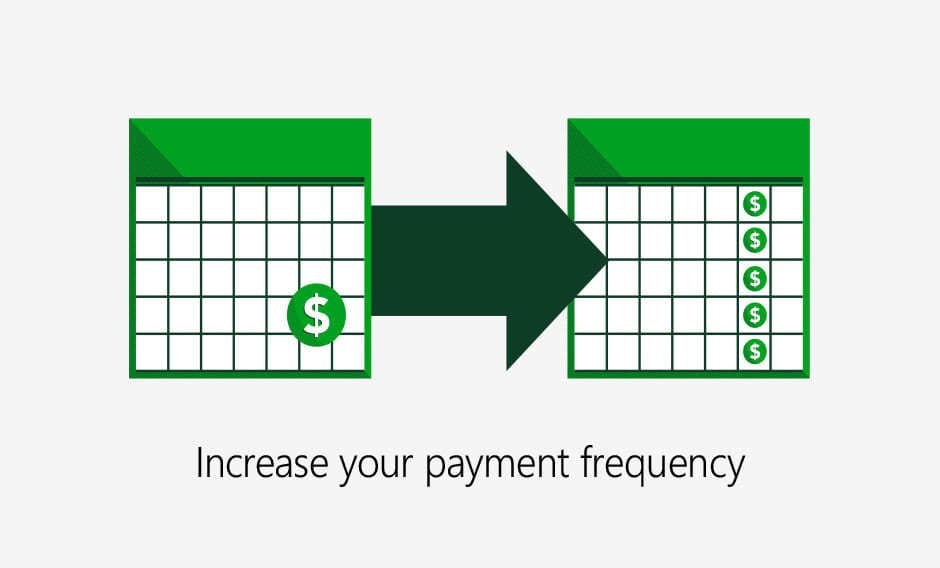

Speed it up

You can pay more often by increasing your principal and interest payments from monthly to rapid weekly or even bi-weekly. Over time, more frequent principal and interest payments will mean that you are paying your TD Mortgage faster.

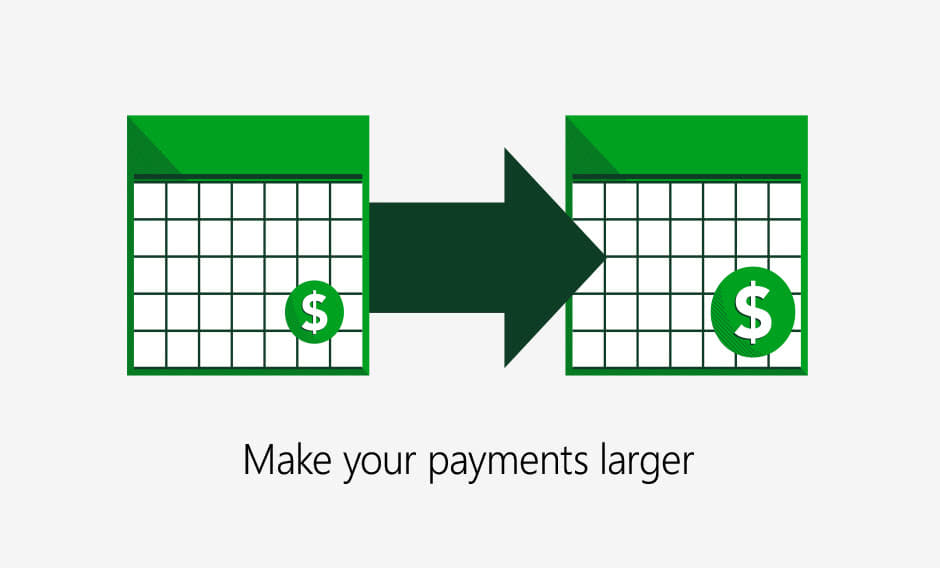

Increase your payment

With TD, you can increase your original scheduled principal and interest payments by up to 100% during your mortgage term. That’s double your normal payment amount. For example, if you typically pay $1,000 a month, you can increase your payment up to $2,000 a month during your mortgage term.

Make a lump sum payment

Got some extra cash? Use it to prepay a bit of your closed TD Mortgage and shrink the amount you owe, faster. Make a lump sum payment of up to 15% of the original principal amount borrowed once per year, free of any prepayment charges. You can prepay as much as you like to reduce your principal if you have an open TD Mortgage.

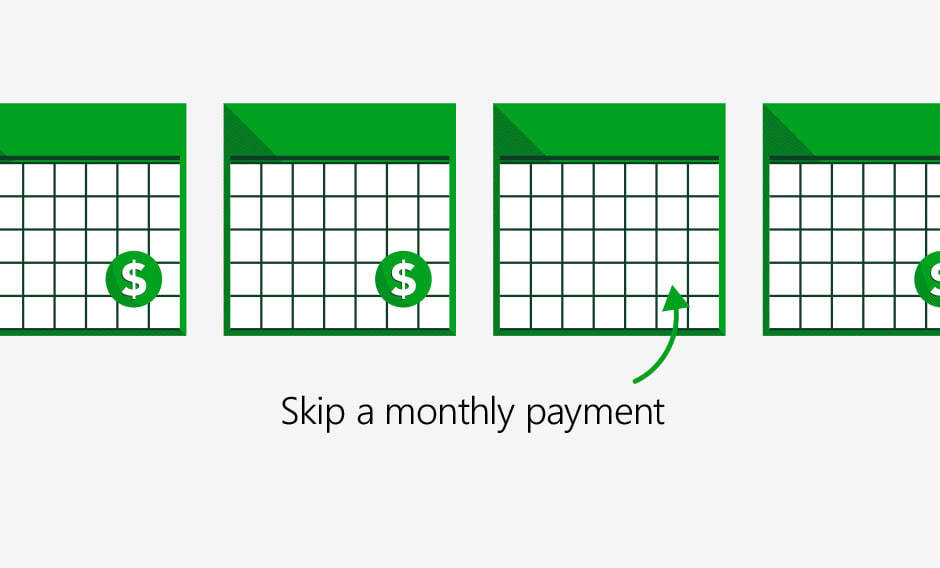

Payment pause

If you need to take an emergency break from your payments, you can request to skip the equivalent of one monthly payment, partially or in full. This can be requested no more than once a calendar year, up to four times over the length of your amortization period.1

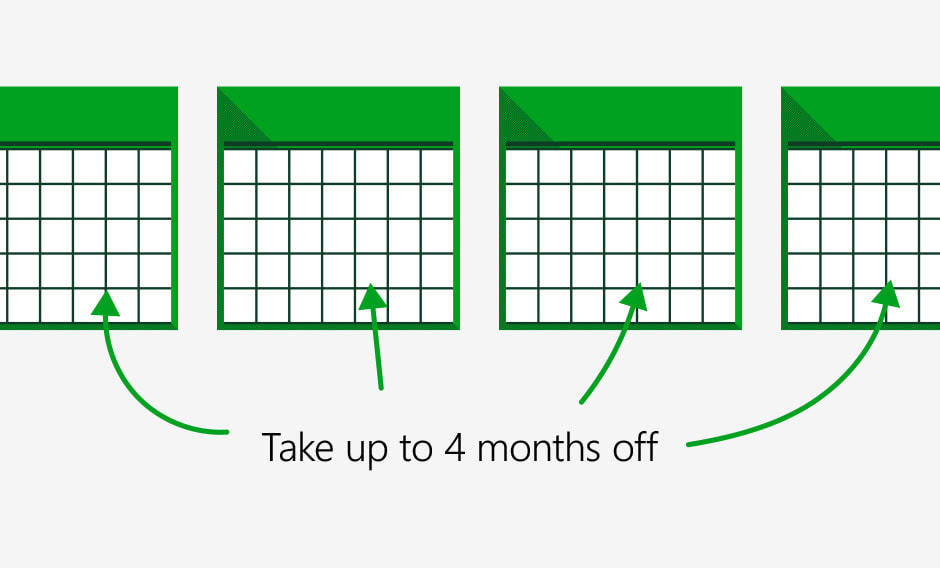

Payment vacation

If you know change is on its way, you can prepare by prepaying in advance. Request to take up to four months off your payments, partially or in full, if you have a prepaid amount that has reduced your amortization schedule. Prepayments can be made by either lump-sum payments towards your principal balance or by increasing your regular payments.1

Legal

1Subject to TD approval. Interest will continue to accrue during this period.

What is a prepayment?

Want to know how a prepayment is different from a principal and interest payment? A prepayment is a lump sum payment of any amount in addition to regular scheduled payments. Like it sounds, prepayment means paying your debt down early.

Whether you make one or multiple lump sum payments, a mortgage prepayment on the principal amount leaves you with a smaller debt, and over time, less interest to pay.

Is a prepayment the right choice for you?

-

Check your terms.

Closed mortgages often have clauses to define how much you can prepay and how often. Paying more than your TD Mortgage loan agreement specifies might result in charges. An open mortgage is structured to allow prepayments anytime, in any amount, without charge. -

Benefits.

Prepayments are a great way to reduce the amount of interest you'll pay overall. The quicker you pay your principal, the less interest you pay. So if you can make a lump sum prepayment, you're ahead of the game. -

When it makes sense.

Prepayments are a great option if you earn a commission or a yearly bonus. If you are free of debt, have an emergency fund, and are a regular contributor to your retirement savings plan, then mortgage prepayment is the next step to consider. -

Charges.

The following actions may result in you having to pay a prepayment charge:

- Paying more than your prepayment privileges allow

- Refinancing (increasing your borrowing amount) before the end of term

- Early renewing your mortgage

- Transferring your mortgage to another lender before the end of your term

Mortgage calculators and tools

Other useful information

Related articles

Let’s connect

Mortgages

Get personalized

advice